Geneva. 12 June 2022. The International Air Transport Association (IATA) announced that air travel resumed its strong recovery trend in April, despite the war in Ukraine and travel restrictions in China. This was driven primarily by international demand.

Note: We have returned to year-on-year traffic comparisons, instead of comparisons with the 2019 period, unless otherwise noted. Owing to the low traffic base in 2021, some markets will show very high year-on-year growth rates, even if the size of these markets is still significantly smaller than they were in 2019.

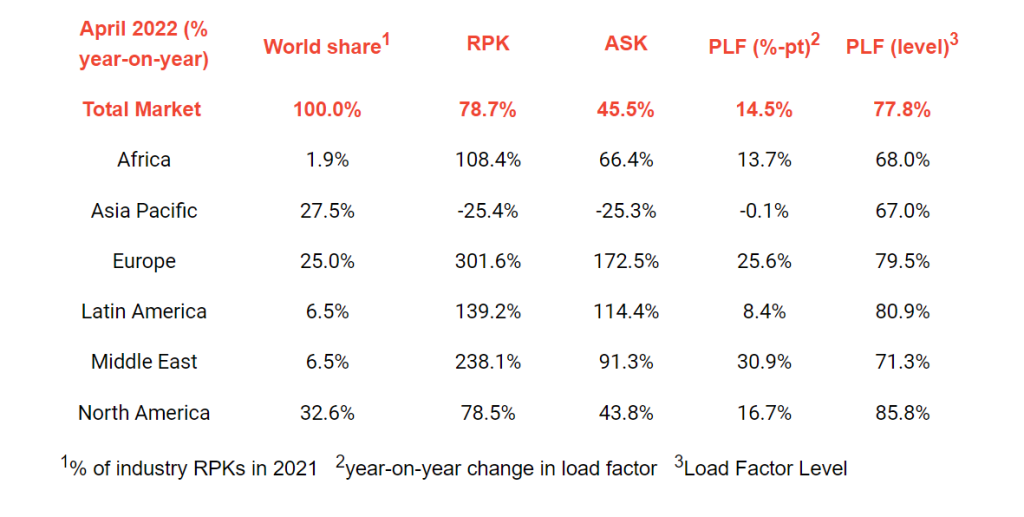

- Total demand for air travel in April 2022 (measured in revenue passenger kilometers or RPKs) was up 78.7% compared to April 2021 and slightly ahead of March 2022’s 76.0% year-over-year increase.

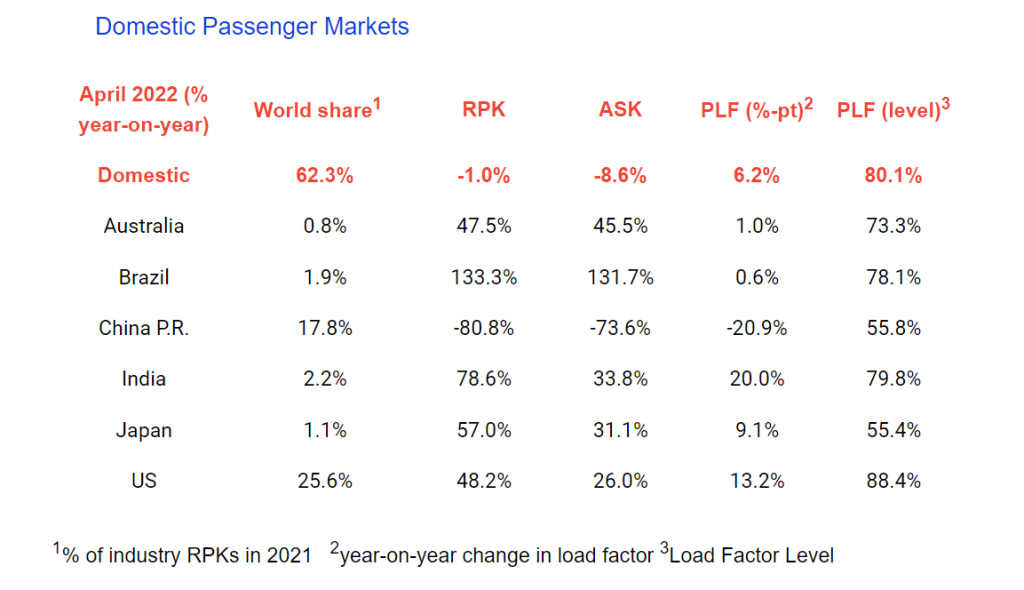

- April domestic air travel was down 1.0% compared to the year-ago period, a reversal from the 10.6% demand rise in March. This was driven entirely by continuing strict travel restrictions in China, where domestic traffic was down 80.8% year-to-year. Overall, April domestic traffic was down 25.8% versus April 2019.

- International RPKs rose 331.9% versus April 2021, an acceleration over the 289.9% rise in March 2022 compared to a year ago. Several route areas are actually above pre-pandemic levels, including Europe – Central America, Middle East – North America and North America – Central America. April 2022 international RPKs were down 43.4% compared to the same month in 2019.

International Passenger Markets

- European carriers’ April international traffic rose 480.0% versus April 2021, substantially up over the 434.3% increase in March 2022 versus the same month in 2021. Capacity rose 233.5% and load factor climbed 33.7 percentage points to 79.4%.

- Asia-Pacific airlines saw their April international traffic climb 290.8% compared to April 2021, significantly improved on the 197.2% gain registered in March 2022 versus March 2021. Capacity rose 88.6% and the load factor was up 34.6 percentage points to 66.8%, still the lowest among regions.

- Middle Eastern airlines had a 265.0% demand rise in April compared to April 2021, bettering the 252.7% increase in March 2022, versus the same month in 2021. April capacity rose 101.0% versus the year-ago period, and load factor climbed 32.2 percentage points to 71.7%.

- North American carriers’ April traffic rose 230.2% versus the 2021 period, slightly above the 227.9% rise in March 2022 compared to March 2021. Capacity rose 98.5%, and load factor climbed 31.6 percentage points to 79.3%.

- Latin American airlines experienced a 263.2% rise in April traffic, compared to the same month in 2021, exceeding the 241.2% rise in March 2022 over March 2021. April capacity rose 189.1% and load factor increased 16.8 percentage points to 82.3%, which easily was the highest load factor among the regions for the 19th consecutive month.

- African airlines’ traffic rose 116.2% in April 2022 versus a year ago, an acceleration over the 93.3% year-over-year increase recorded in March 2022. April 2022 capacity was up 65.7% and load factor climbed 15.7 percentage points to 67.3%.

- Australia’s domestic demand rose 47.5% compared to April 2021, an improvement over the 36.5% rise in March traffic, owing to the lifting of travel restrictions and rising consumer confidence.

- Japan likewise saw monthly gains, with domestic RPKs up 57.0% year-over-year, up from a 46.5% rise in March 2022 compared to March 2021.

2022 vs 2019

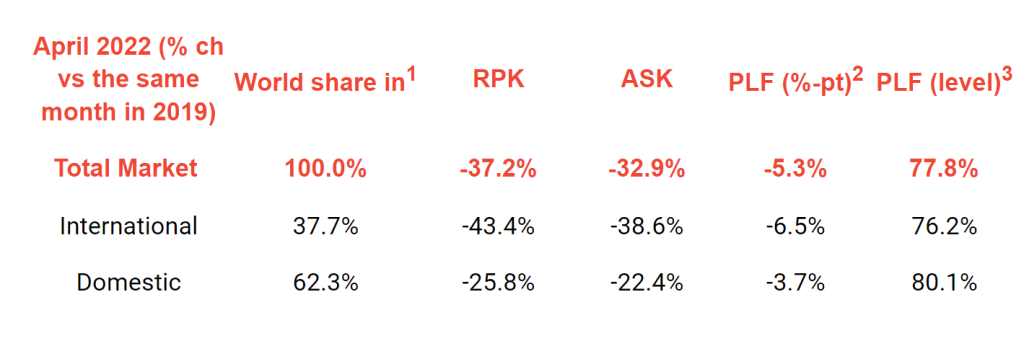

Total April passenger demand was down 37.2% compared to the same month in 2019, which is an improvement compared to the 41.3% decline for March 2022 versus March 2019.

The Bottom Line

“With the northern summer travel season now upon us, two things are clear: two-years of border restrictions have not weakened the desire for the freedom to travel. Where it is permitted, demand rapidly is returning to pre-COVID levels. However, it is also evident that the failings in how governments managed the pandemic have continued into the recovery. With governments making U-turns and policy changes there was uncertainty until the last minute, leaving little time to restart an industry that was largely dormant for two years. It is no wonder that we are seeing operational delays in some locations. In those few locations where these problems are recurring, solutions need to be found so passengers can travel with confidence.

“In less than two weeks, leaders of the global aviation community will gather in Doha at the 78th IATA Annual General Meeting (AGM) and World Air Transport Summit. This year’s AGM will take place as a wholly in-person event for the first time since 2019. It should send a strong signal that it is time for governments to lift any remaining restrictions and requirements and prepare for an enthusiastic response by consumers who are voting with their feet for a full restoration of their right to travel,” said Walsh.

-A4-Size-(2)_page-0001.jpg)